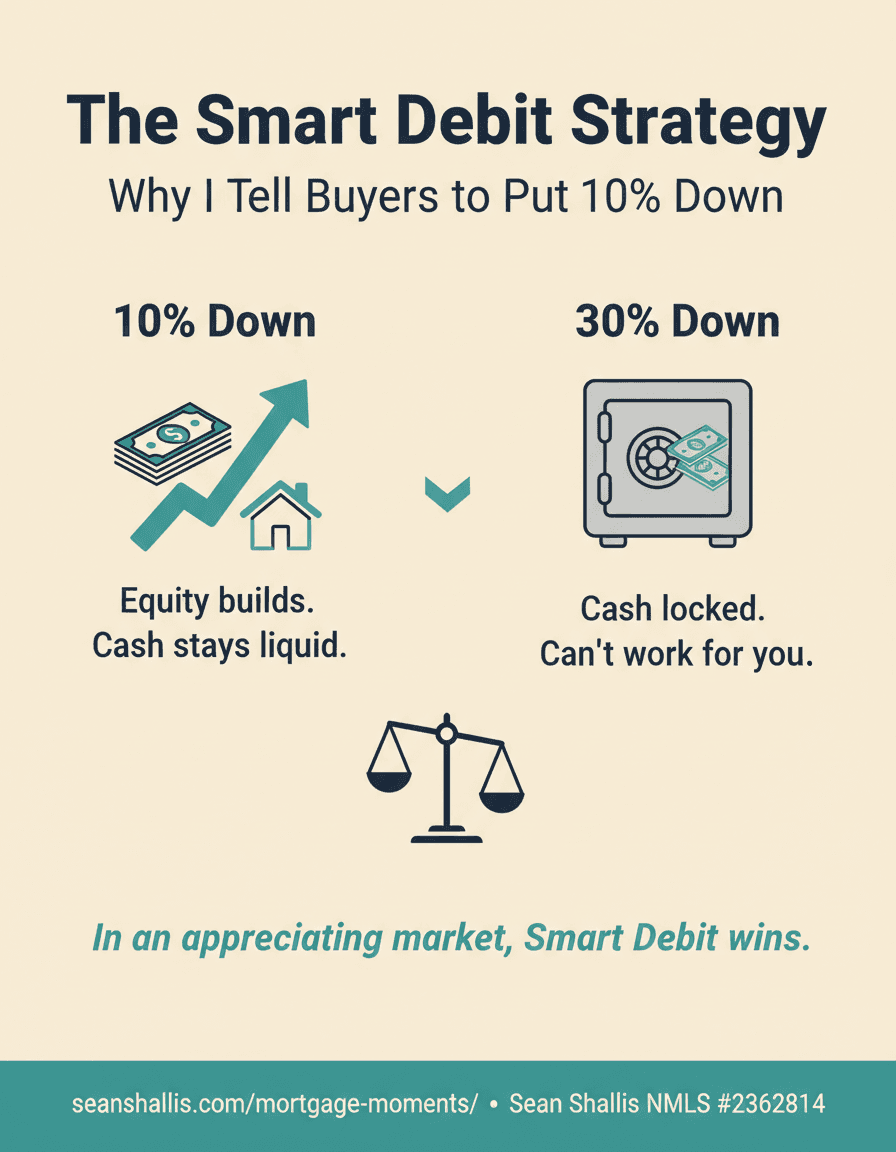

The Smart Debit Strategy: Why I Tell Buyers to Put 10% Down

A buyer reached out this week with a question I hear constantly — and it's one that most mortgage advice gets completely backwards.

The Question That Sparked This Post

“If I put only 10% then I will have to pay more monthly right? And it takes a long time to clear it.”

It's a fair question. On the surface, putting less down means a bigger loan balance, which means a higher monthly payment. That part is true. But the question underneath the question — the one that actually matters — is: what's the smartest use of your cash right now?

And when I look at that question honestly, my answer is almost always the same: put less down, not more.

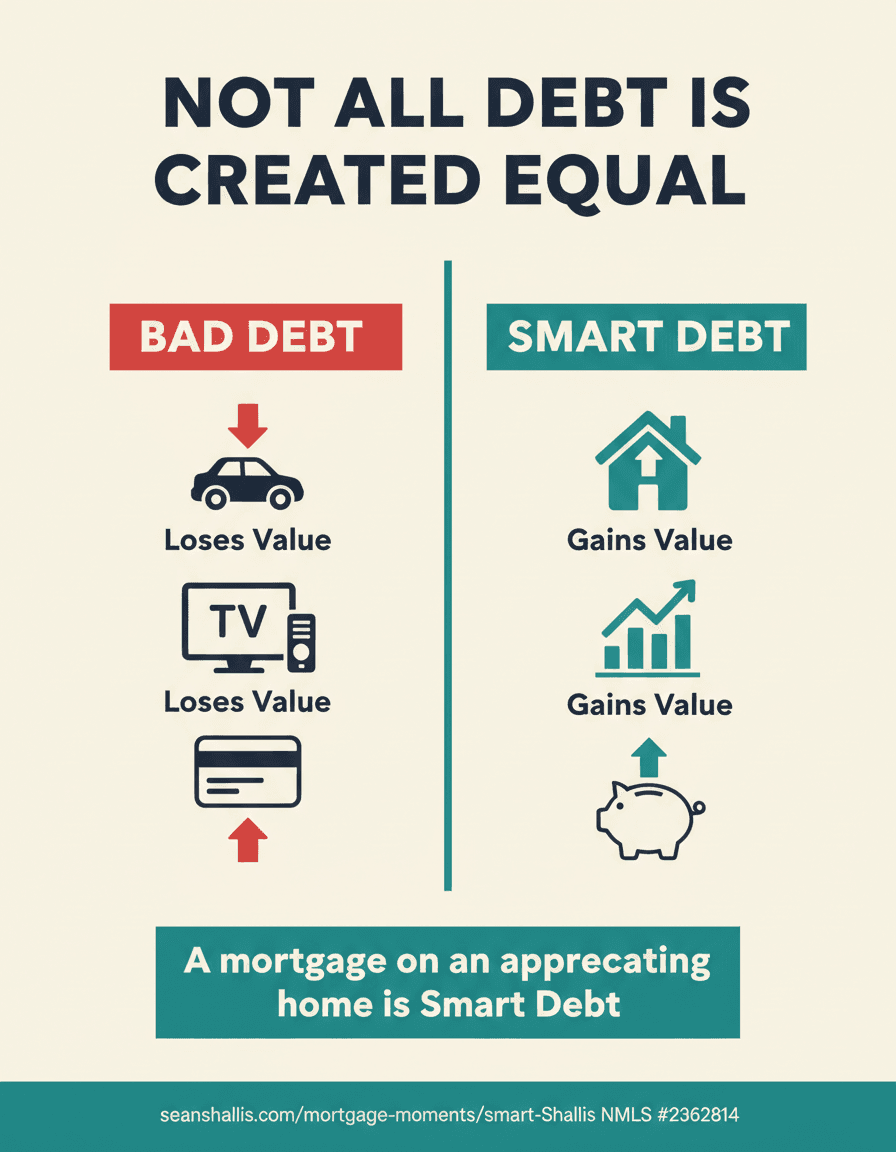

Good Debt vs. Bad Debt

There's a concept I call Smart Debit— borrowing against an asset that grows in value over time. It's the opposite of bad debt, which is borrowing to buy something that depreciates the moment you sign the papers.

A mortgage on a home in an appreciating market is Smart Debit. The property goes up in value whether you put 10% down or 30% down. Your equity grows either way. But if you put 30% down, you've locked up a large chunk of cash inside four walls where it earns you nothing liquid.

That's the part people miss. Equity in a home is not a savings account. You can't access it without refinancing or selling. It doesn't compound. It just sits there — growing with the market, yes, but completely illiquid.

The Leverage Advantage

Here's the framework I walk buyers through. Imagine two buyers — both purchasing the same $500,000 home in a market that appreciates 5% per year.

Both buyers captured the same $25,000 in appreciation. The home doesn't care how much you put down — it grows the same either way. But Buyer B kept $50,000 liquid. That cash can sit in a high-yield savings account earning 4–5%, can go toward the right investment, or can cover a major repair without touching the mortgage.

That's leverage working for you. You're controlling a $500,000 appreciating asset with $50,000 instead of $100,000. Your return on capital is effectively doubled.

What About the Higher Payment?

Yes — 10% down means a slightly higher monthly payment than 20% down. That's real, and it matters. The question is whether you can comfortably afford it.

If a buyer can make the payment at 10% down without financial stress, then the Smart Debit case is strong. If the payment at 10% down is a stretch, that's a different conversation — and putting more down to get the payment right is completely valid.

There's one more condition worth noting: the rate shouldn't change. In some loan scenarios, going from 20% to 10% down triggers a pricing adjustment. If the rate stays the same, the math tilts clearly toward 10% down. If it costs you in rate, we need to run the actual numbers.

Three Practical Takeaways

Use leverage in appreciating markets

Your home gains value based on the full purchase price — not your down payment. Putting less down doesn't change how much the property grows. It frees up capital to work elsewhere.

Keep the difference liquid

The 10% you didn't put down belongs in a high-yield savings account or a sound investment — not spent. Think of it as a reserve that earns, not a windfall.

Extra payments go straight to principal

If you want to pay down the loan faster, you always have the option of adding extra to your monthly payment. Every dollar above the minimum goes directly to principal — shortening the loan and building equity on your terms.

The Bottom Line

Putting 10% down isn't settling. In the right market, with the right payment comfort level, it's the smarter move. You're not "paying more" in the way most people fear — you're deploying capital strategically. The house still grows. Your savings still grow. And you still have options.

The goal isn't to minimize your loan balance as fast as possible. The goal is to build wealth — and Smart Debit, used wisely, is one of the best tools for doing exactly that.

Mortgage Moments

Have a question of your own?

Ask Rosie for a free rate check, or book a call with Sean to walk through your specific situation — down payment, loan structure, and all.

Sean Shallis · Mortgage Loan Originator · NMLS #2362814. This post is for educational purposes only and does not constitute financial or mortgage advice. All loan scenarios are illustrative. Actual rates, payments, and qualification depend on your individual financial profile, creditworthiness, property, and loan program. Contact Sean for a personalized analysis. Equal Housing Lender.