The $250 Reset: How to Lower Your Monthly Payment Without Refinancing

Most homeowners have never heard of this. One lump sum payment, a $250 fee, and your lender recalculates your entire amortization schedule — lower monthly payment, same rate, same payoff date, zero closing costs.

The Question That Sparked This Post

“I heard that if we make a lump sum payment to the mortgage, we can pay $250 and adjust our remaining payments downward — is that right?”

That's exactly right — and the fact that most homeowners have never heard of it is one of the most expensive gaps in mortgage education. It's called a recast, and it's one of the most underused tools available to borrowers who want to lower their monthly obligation without touching their rate or restarting their loan.

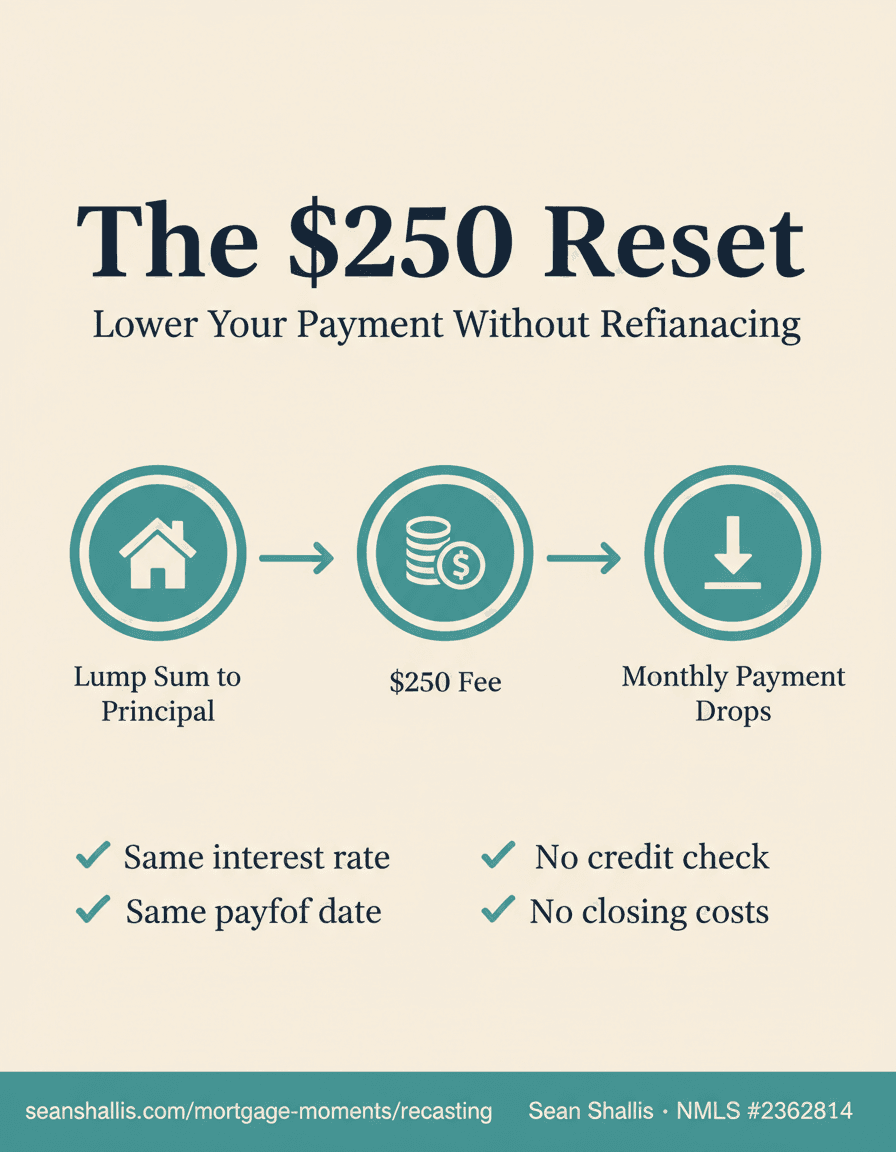

What Is a Mortgage Recast?

A recast (sometimes called re-amortization) is simple: you make a significant lump sum payment directly toward your principal balance. Then you pay your lender a small administrative fee — typically around $250 — and they recalculate your monthly payment based on the new, lower balance over the remaining term of your loan.

Everything else stays exactly the same. Your interest rate doesn't change. Your loan term doesn't reset. There's no credit check, no appraisal, no underwriting, no closing costs. You simply owe less principal — so your required monthly payment goes down to reflect that.

How a Recast Works

Make a lump sum principal payment

Bonus, inheritance, sale proceeds, savings — any large sum applied directly to your balance.

Request a recast from your lender

A simple written request. Most conventional loans allow it; confirm with your servicer.

Pay the recast fee

Typically ~$250. No appraisal. No credit pull. No closing costs.

Receive your new lower payment

Your lender re-amortizes the remaining balance over the remaining term. Same rate, same payoff date — just a smaller required monthly payment.

A Real Example

Let's say you have a $600,000 mortgage at 6.5% with 25 years remaining. Your current payment is roughly $4,056/month. You receive a $75,000 bonus and apply it to your principal.

That's roughly $507 less per month — permanently — for a one-time $250 fee. No refinance. No new closing costs. No rate risk. The math is almost always favorable if you have the lump sum available.

Recast vs. Refinance — What's the Difference?

A refinance replaces your loan with a new one — new rate, new term, new closing costs (typically 2–3% of the loan balance), new credit inquiry. It makes sense when rates have dropped significantly below what you're currently paying and the savings justify the cost.

A recast doesn't touch any of that. It's purely a recalculation of your existing loan's payment schedule based on a lower balance. There's no rate improvement — but if your current rate is already competitive, that's fine. You're not chasing a better rate. You're converting a lump sum into permanent monthly relief.

When to recast

You have a lump sum (bonus, inheritance, home sale proceeds) and want to reduce your required monthly payment. Your current rate is reasonable and you're not looking to change terms — just lower the obligation.

When to refinance

Rates have dropped materially below your current rate and the long-term savings justify the closing costs. Or you want to change your loan term — move from 30 to 15 years, for example.

When to do both over time

Recast now to lower your payment. Refinance later if rates drop enough to make it worth it. These aren't mutually exclusive — they're tools for different moments.

A Few Things to Know First

Not every loan is recast-eligible. Conventional loans (Fannie Mae and Freddie Mac) typically allow it. FHA and VA loans generally do not. Jumbo loans vary by lender. Before you plan around a recast, confirm eligibility with your servicer.

Most lenders also require a minimum lump sum — often $5,000 to $10,000 — before they'll process a recast. The math needs to move the needle enough to be worth their administrative effort.

And one more thing worth noting: a recast lowers your requiredmonthly payment — your floor. It doesn't stop you from continuing to pay more. If you want to keep accelerating the payoff, you can keep making larger payments. The recast just gives you breathing room when you need it.

The Bottom Line

If you've come into a lump sum and you're trying to decide what to do with it, a recast deserves serious consideration — especially if your rate is already competitive and a refinance doesn't pencil out. For $250 and a phone call to your servicer, you can permanently reduce your monthly housing cost, keep your existing rate, and preserve every year you've already paid down.

Most homeowners never ask about this option. Now you know it exists.

Mortgage Moments

Want to know if a recast makes sense for your loan?

Ask Rosie to run the numbers on your specific situation — or book a call with Sean to walk through whether a recast, a refinance, or a combination of both is the right move.

Sean Shallis · Mortgage Loan Originator · NMLS #2362814. This post is for educational purposes only and does not constitute financial or mortgage advice. Payment examples are illustrative and based on approximate figures. Recast eligibility, fees, and minimum payment requirements vary by lender and loan type. Confirm details with your loan servicer. Contact Sean for a personalized analysis. Equal Housing Lender.