ARM or Fixed? The Answer Most Loan Officers Won't Give You

Most loan officers give you the safe answer. Here's how to actually decide — based on your timeline, your cash flow, and where rates are in the cycle.

The Question That Sparked This Post

“My loan officer just told me to go with a 30-year fixed. But rates are high right now — shouldn't I consider an ARM? Am I missing something?”

You're not missing something. You're asking exactly the right question — and the fact that your loan officer didn't engage with it seriously is worth noting.

The 30-year fixed is the default answer because it's the safe answer. Safe for the lender. Safe for the loan officer who doesn't want to explain anything complicated. But it isn't always the right answer for you. Let me give you the actual framework.

What an ARM Actually Is

An adjustable-rate mortgage starts with a fixed rate for an initial period — typically 5, 7, or 10 years — then adjusts annually based on a market index. The initial rate is almost always lower than a comparable 30-year fixed.

The trade-off: your payment can change after that initial period ends. That's where most people stop reading. But the story doesn't end there.

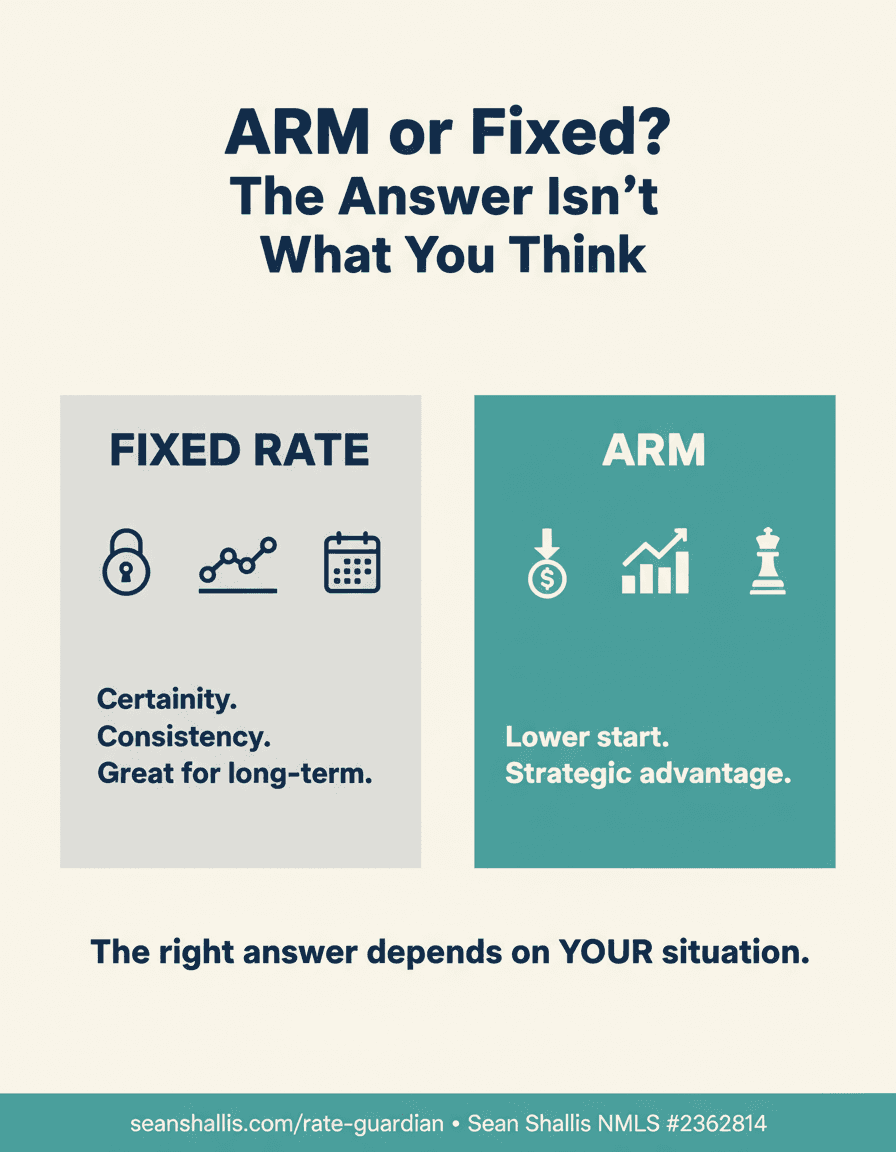

The Case for Fixed

A 30-year fixed gives you certainty. Your rate and payment never change, no matter what happens to interest rates over the next three decades. If you're buying your forever home, planning to stay long-term, or value predictability above all else — fixed is the right call. Predictability has real value, especially when your income, family size, or career are still in motion.

The Case for ARM — When It Actually Makes Sense

Here's what most people miss: the initial fixed period of an ARM is often where most of the financial benefit sits.

On a 7/1 ARM, you're locked into a lower rate for seven years. That means:

Lower monthly payment during those seven years

More of each payment goes to principal early — when it matters most

Meaningful interest savings over that window, often tens of thousands of dollars

If you're a physician in residency buying your first home — if you're a professional who expects to relocate in five to seven years — if you're a high-income buyer who plans to pay down aggressively or refinance strategically — an ARM can be the smarter financial move.

The risk only materializes if you're still in the loan when the adjustment period hits. If your plan accounts for that, the risk largely disappears.

The Three Questions That Actually Decide It

Before choosing, answer these honestly:

How long do you actually plan to stay?

If under seven years — strongly consider an ARM. If 15+ years — fixed likely wins. If you're genuinely unsure, that uncertainty itself is useful data.

What does your cash flow look like right now?

A lower initial ARM payment frees up cash for investments, debt paydown, or building reserves. If that flexibility matters to your broader financial picture, it's worth quantifying.

Where are rates in the cycle?

When rates are high relative to historical norms, ARMs carry less risk — adjustments are more likely to move sideways or down than further up. Context matters. (Note: this is not a prediction about future rate movement — no one can guarantee that.)

What I Actually Tell Clients

I don't have a default answer. I run the numbers for your specific scenario — purchase price, down payment, income trajectory, timeline, cash flow — and show you what each option looks like over 5, 7, and 10 years.

Sometimes the math is close. Sometimes one option wins decisively. Either way, you deserve to see the analysis, not just the easy answer.

Results vary by loan, rate environment, and individual financial situation. This is educational content — not a rate quote or commitment to lend. Let's run your specific numbers.

The Bottom Line

ARM or fixed isn't a personality test. It's a math problem with a few key variables: how long you're staying, what your cash flow looks like, and where rates are when you're buying.

Any loan officer who answers that question without asking those three things first is giving you their default — not your optimal.

Mortgage Moments

Want to see the actual comparison for your situation?

I'll run both scenarios side by side so you can decide with full information — not just the easy answer.

Sean Shallis · Mortgage Loan Originator · NMLS #2362814. This post is for educational purposes only and does not constitute financial or mortgage advice. ARM products vary by lender, loan program, and market conditions. Rate adjustments after the initial fixed period are subject to index changes and loan caps. All examples are illustrative. Contact Sean for a personalized analysis of your specific situation. Equal Housing Lender.