The 30-Year Freedom Strategy: Why Flexibility Beats a Shorter Term

Most people think a shorter loan term means faster freedom. Here's the math — and the legal reality in New Jersey — that changes the whole conversation.

The Question That Sparked This Post

“What did you mean by flexibility in your email? Isn't a 30-year just paying more interest for longer?”

It's the right question — and the answer unlocks one of the most powerful tools in mortgage strategy. Yes, a 30-year loan has a lower required monthly payment than a 15-year. But that doesn't mean you have to pay it off in 30 years. Not even close.

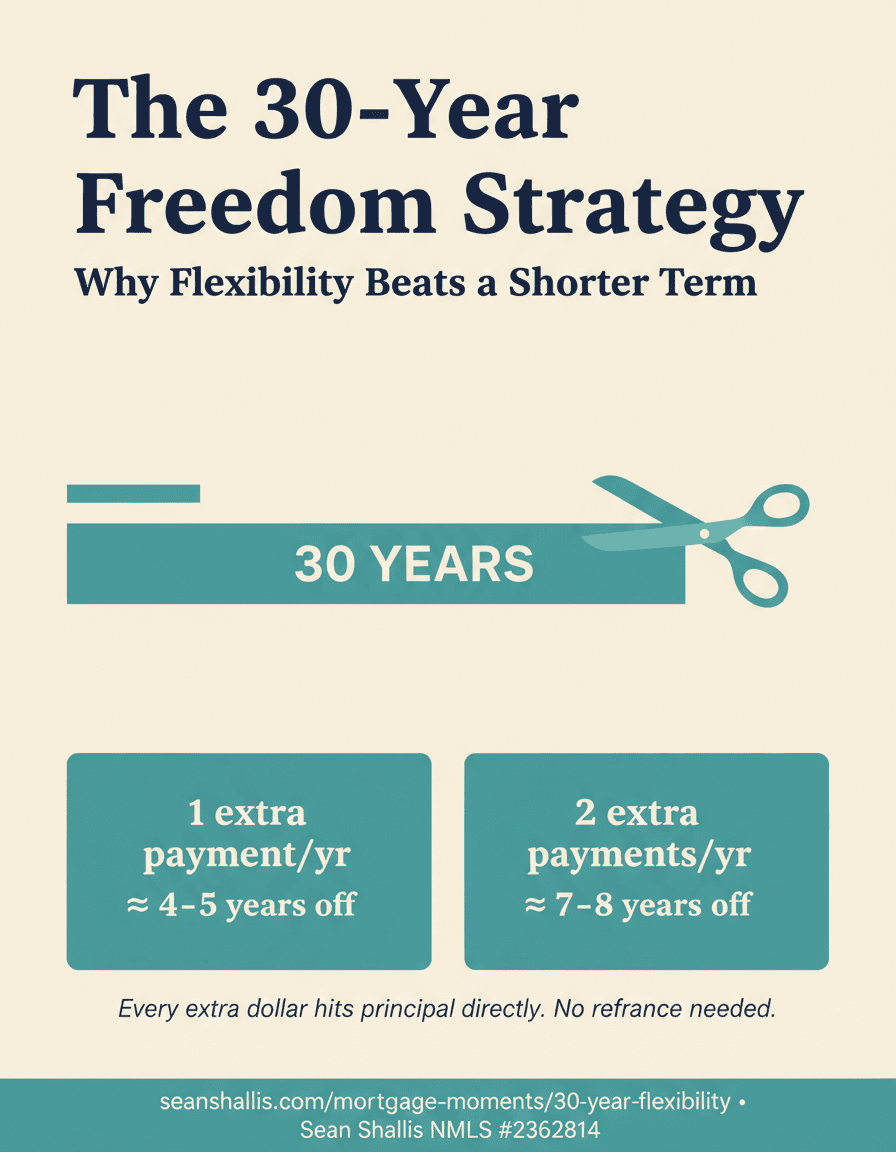

What One Extra Payment a Year Actually Does

Making just one extra mortgage payment per year on a standard 30-year fixed loan knocks roughly 4–5 years off the back end. You'd pay off your home in about 25–26 years instead of 30 — and save a significant chunk of interest along the way.

Bump it to two extra payments a yearand you're looking at roughly 7–8 years shaved off — paid off near year 22 or 23.

Why does this work so dramatically? Every extra dollar you send in hits principal directly. Less principal means less balance to charge interest on — and since mortgage interest compounds daily on your remaining balance, shrinking that balance early has an outsized effect on the total cost of the loan. Same rate. No refinance. No fee. Just faster freedom.

The New Jersey Factor: Prepayment Penalties Are Illegal

Here's the part most people don't know — and it's a big one. In New Jersey, prepayment penalties on residential mortgages are illegalin most cases. And NJ isn't alone — the majority of states have abolished or severely restricted prepayment penalties on standard home loans.

That means your lender cannotcharge you a fee for paying ahead. There's no penalty for sending in an extra payment. No form to fill out. No permission to ask for. You just pay more — and every extra dollar goes straight to the principal balance.

This legal reality is exactly why I almost always recommend the 30-year over the 15-year for the right buyer.

What I Mean by Flexibility

A 15-year mortgage locks you into a higher required payment every single month — good months and bad months alike. Miss it, and you're in default territory. Life doesn't work on a fixed schedule, and locking yourself into a higher mandatory payment is a form of financial rigidity most people underestimate.

A 30-year loan gives you a lower minimum payment — but you control the throttle. On months where you have extra cash — a bonus, a commission check, a tax refund, a strong sales month — you make a bigger payment. That extra goes straight to principal, shortening your loan and saving interest.

On months where life happens — a car repair, a medical bill, a trip with the family, a slow business month — you make the minimum payment. You don't fall behind. You don't stress. You stay protected.

That's the flexibility. You build the same equity, pay off the loan on an aggressive timeline, and you never have to choose between your mortgage and a family emergency.

Three Ways to Think About It

Extra payments = accelerated payoff, no fees

Every dollar above the minimum hits principal. No penalty, no paperwork. One extra payment a year can take 4–5 years off your loan. Two can take off 7–8. You decide the pace.

The minimum is your safety net, not your ceiling

The lower 30-year payment is a floor, not a target. Pay it on tight months. Pay more on strong months. The loan doesn't care — it just adjusts your payoff date accordingly.

Prepayment penalties are illegal in NJ — and most states

You cannot be charged for paying early. That changes everything. The 30-year isn't a trap — it's a tool you can wield on your own timeline.

The Bottom Line

The 30-year fixed isn't the slow road. It's the road with an adjustable throttle. You can drive it like a 25-year loan, a 22-year loan, or a 30-year loan — depending on what that month looks like. No refinance, no fee, no permission required.

And in New Jersey — where prepayment penalties on residential mortgages are illegal — you have every legal protection you need to use it exactly this way.

That's what I mean by flexibility. Build the wealth. Keep the options. Own the timeline. That's the 30-year freedom strategy.

Mortgage Moments

Want to run the numbers on your loan?

Ask Rosie for a free rate check, or book a call with Sean to map out exactly how an accelerated payoff strategy would work for your situation.

Sean Shallis · Mortgage Loan Originator · NMLS #2362814. This post is for educational purposes only and does not constitute financial or legal advice. Payoff timelines are approximate and vary based on loan balance, interest rate, and payment amount. Prepayment penalty laws vary by state — consult your loan documents and a licensed professional for guidance specific to your situation. All examples are illustrative. Contact Sean for a personalized analysis. Equal Housing Lender.